Our fees:

$1,000,000 Donation

-$20,000 Credit Card Fees

-$100 Transaction Fees

=$979,900 Donation After Fees

Save $40,000+

in Donations

PWI Fundraising Tools

- Search

- Swipe

- GroupGive

- Crowdfund

- Shopping

- Auction

- Text2Give

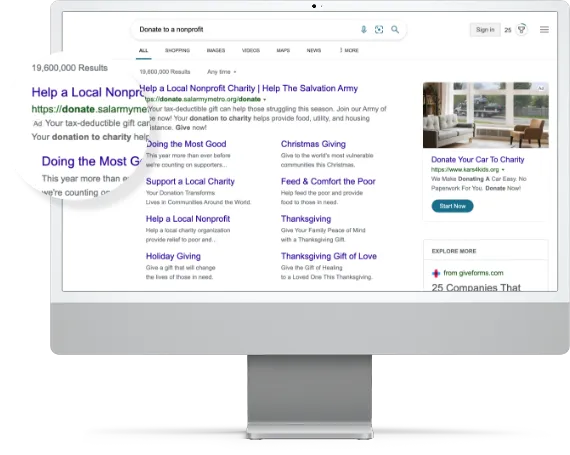

PWI Search

PWI Search functions alongside the PWI Fund browser extension and allows users to simply download the extension and raise money by continuing their regular web browsing.PWI Swipe

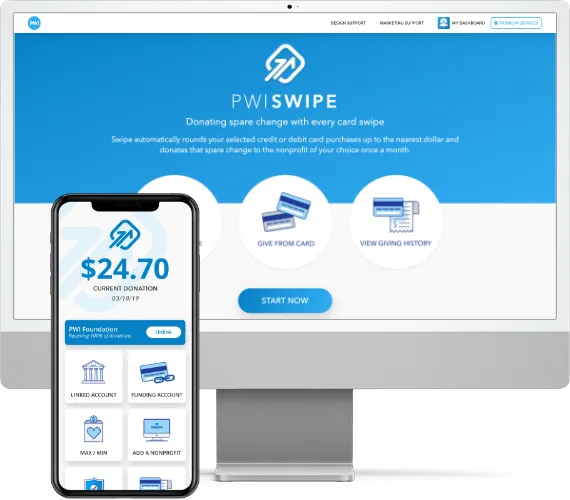

PWI Swipe is fully functional on desktop or mobile. Once a donor sets their credit or debit cards, they won’t need to do anything else to begin donating change from their purchases.PWI GroupGive

PWI Swipe is fully functional on desktop or mobile. Once a donor sets their credit or debit cards, they won’t need to do anything else to begin donating change from their purchases.PWI Crowdfund

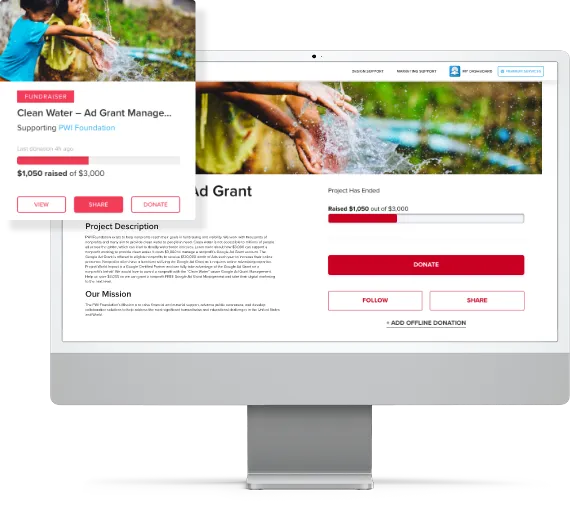

Crowdfunding makes donations tangible—your donors can see a progress bar and share what your organization is doing with their network. The best part? These donations are never conditional, so even if you don’t meet your goal, the money raised will still go to you.PWI Shopping

Shopping functions alongside the PWI Fund browser extension and allows users to simply download the extension and raise money as they shop on all our partnered online stores.PWI Auction

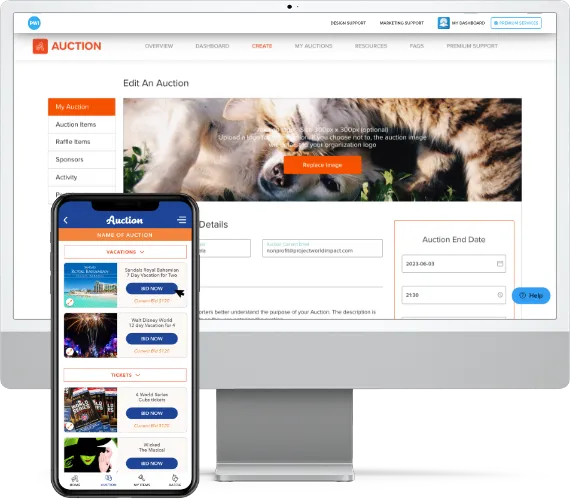

Manage your auction items, track bidding, contact winners, and run your auction on the go. Auction and raffle items can be added individually with descriptions, values, images, and more. Add as many items as you like.PWI Text2Give

PWI Text2Give is a way for your supporters to make meaningful donations, instantly. All you have to do is share your Text2Give code—automatic replies will direct your supporters through the simple donation process.

Additional Plans & Growth Oportunities

Enjoy using Processing on the Free & Basic plans. We have other plans to help give your nonprofit an extra boost.

Free Plan

FREE

2.75% + 25¢

per successful card charge

KEY FEATURES:

- 2.75% + 25¢ per transaction

- Access to free nonprofit tools

Plus Plan

$500/mo

2.33% + 25¢

per successful card charge

KEY FEATURES:

- 2.33% + 25¢ per transaction

- Access to a set of nonprofit tools focused on fundraising, visibility or operations

Pro Plan

$750/mo

2.10% + 15¢

per successful card charge

KEY FEATURES:

- 2.10% +15¢ per transaction

- Access to a complete suite of nonprofit tools

| Comparison Chart |

|

|

|

|

| Processing Fees | 2.10% + 15¢ per transaction | 2.6% + 10¢ per transaction | 2.9% + 30¢ per transaction | 2.9% + 30¢ per transaction |

| ACH Processing Fees | 50¢ per transaction | 1% with a $1 minimum per transaction | NA | 2.9% + 30¢ per transaction |

| Money Availability | 3-5 Days | 1-2 Days | Weekly | 3-5 Days |

| Payment Methods | All major credit cards, ACH | All major credit cards, Apple Pay & Google Pay, ACH | All major credit cards | PayPal Payments, PayPal Credit, and all major credit and debit cards, ACH |

| Sign-up Time | 2-5 minutes | 2-5 minutes | 2-5 minutes | 2-5 minutes |

| Accept Online/In-Person Payments |

|

|

|

|

| Connect Existing Account to PWI Processing |

|

|

|

|

| Scheduled Payments |

|

|

|

|

| Card Swiping |

|

|

|

|

| Convenience Fees |

|

|

|

|

See What Our Users Are Saying About Search